The Bank of England’s Monetary Policy Committee (MPC) opted to hold its benchmark interest rate steady at 3.75% during its initial meeting of 2026, maintaining the rate at its lowest point since February 2023. This decision follows a significant reduction from 4% in December 2025, a move that signalled a potential shift in the Bank’s stance after a prolonged period of tightening. However, financial analysts and market participants remain sharply divided on the likely pace and frequency of any further rate reductions throughout the year. The trajectory of interest rates holds profound implications for millions across the UK, directly impacting mortgage payments, credit card debt, and the returns on savings.

Understanding Interest Rates and Their Dynamics

At its core, an interest rate represents the cost of borrowing money or the reward for saving it. The Bank of England’s base rate is the foundational interest rate, influencing what commercial banks and building societies charge each other for overnight lending. In turn, this cascades down to the rates they offer their customers for various financial products, including mortgages, personal loans, and savings accounts.

The primary mandate of the Bank of England is to maintain price stability, specifically by keeping inflation at its 2% target. When inflation, as measured by the Consumer Price Index (CPI), consistently exceeds this target, the Bank typically responds by raising the base rate. The rationale behind this tightening monetary policy is to make borrowing more expensive and saving more attractive, thereby discouraging spending and reducing overall demand for goods and services. This reduction in demand is intended to alleviate upward pressure on prices, bringing inflation back down towards the target. Conversely, when inflation is under control and economic growth slows, the Bank may consider cutting rates to stimulate economic activity by making borrowing cheaper and encouraging investment and consumption. Other factors considered by the MPC include unemployment levels, wage growth, and broader global economic conditions.

The UK’s Recent Inflation and Interest Rate Journey

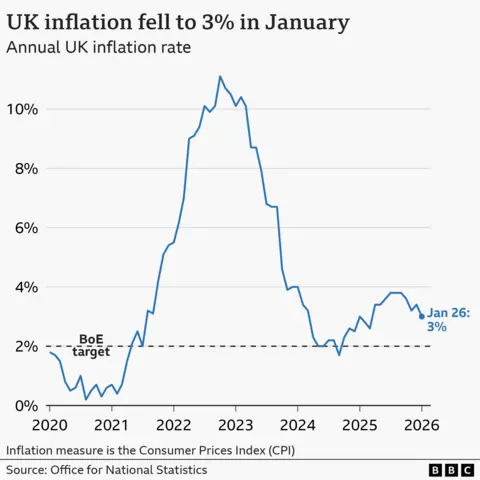

The UK economy has experienced a tumultuous period of high inflation in recent years. The main inflation measure, CPI, soared to a peak of 11.1% in October 2022, a level not seen in decades. This surge was primarily driven by a confluence of factors including post-pandemic supply chain disruptions, a sharp rebound in consumer demand, and the significant increase in energy and food prices exacerbated by Russia’s invasion of Ukraine.

In response to this inflationary spiral, the Bank of England embarked on a series of aggressive rate hikes, pushing the base rate from historic lows to a recent high of 5.25% in 2023. This level was maintained for several months, reflecting the MPC’s commitment to taming persistent price rises. The turning point arrived in August 2024, when the Bank initiated its first rate cut, a sign that the worst of the inflation crisis might be over. The subsequent cut to 4% in December 2025 and the current hold at 3.75% in January 2026 reflect a cautious approach to normalising monetary policy.

Encouragingly, the Office for National Statistics (ONS) reported a significant deceleration in inflation. The fall was notably attributed to easing pressures on fuel costs, a stabilisation in food prices, and more competitive airfares. In the year to January 2026, CPI inflation registered at 3%, a notable decrease from 3.4% the previous month. While still above the 2% target, this downward trend provides the Bank with greater flexibility to consider further rate adjustments. The sustained decline in inflation is the primary catalyst making additional rate cuts increasingly probable.

Outlook: The Prospect of Further Rate Cuts

The recent MPC meetings have highlighted a clear division within the nine-member committee regarding the optimal path for interest rates. Both the December 2025 rate cut and the January 2026 decision to hold rates were passed by a narrow 5-4 vote. This split underscores the ongoing debate among policymakers regarding the balance of risks: cutting too soon could reignite inflation, while holding too long could stifle economic growth.

Following the January decision, Bank of England Governor Andrew Bailey offered a cautiously optimistic outlook. He stated, "We now think that inflation will fall back to around 2% by the spring. That’s good news. We need to make sure that inflation stays there." He further added a conditional note, "All going well, there should be scope for some further reduction in the Bank rate this year." This forward guidance suggests that while the Bank is open to further easing, its decisions will remain data-dependent, contingent on inflation continuing its downward trajectory and avoiding any unforeseen economic shocks.

Market analysts and economists are largely anticipating one or two additional rate cuts during 2026. Speculation is rife among traders, with some even forecasting a potential first cut as early as the next MPC meeting on 19 March. This anticipation is fueled by ongoing disinflationary trends and a desire to support an economy that has faced significant headwinds. However, the exact timing and magnitude of these cuts will hinge on crucial economic data releases, including future inflation figures, wage growth statistics, employment reports, and retail sales performance. The Bank’s ultimate goal is to achieve a "soft landing" – bringing inflation back to target without precipitating a severe economic downturn or recession.

Impact of Rate Cuts on Mortgages, Loans, and Savings

The Bank of England’s interest rate decisions have far-reaching implications for household finances across the UK.

Mortgages: Approximately 500,000 homeowners hold tracker mortgages, which are directly linked to the Bank’s base rate. Any reduction in the base rate will lead to an immediate decrease in their monthly repayments, offering welcome relief. A similar number of homeowners are on standard variable rates (SVRs), where lenders typically, though not always immediately, pass on Bank rate cuts.

However, the vast majority of mortgage customers are on fixed-rate deals. For these individuals, current monthly payments remain unaffected by immediate rate changes. The real impact is felt when their fixed-rate terms expire. As of 18 February 2026, the average two-year fixed residential mortgage rate stood at 4.85%, while a five-year fixed rate was 4.97%, according to financial information company Moneyfacts. The average two-year tracker rate was 4.44%, reflecting the direct link to the base rate. A critical concern is the estimated 800,000 fixed-rate mortgages with interest rates of 3% or below that are scheduled to expire annually until the end of 2027. Borrowers coming off these historically low rates are expected to face significantly higher repayments, creating a substantial "mortgage cliff edge" for many households. Future rate cuts could help to mitigate the severity of these increases, making new fixed-rate deals more affordable.

Other Loans: The Bank of England’s base rate also influences the interest rates charged on other forms of credit, such as credit cards, personal bank loans, and car financing. While lenders can decide to reduce their own interest rates as their borrowing costs fall, this transmission mechanism tends to be slower and less direct than with tracker mortgages. Lenders may be slower to pass on benefits to borrowers and quicker to adjust savings rates downwards. Nevertheless, a trend of falling base rates generally translates to cheaper borrowing costs for consumers over time, potentially stimulating consumer spending and investment.

Savings Rates: For savers, a falling base rate generally signals a reduction in the returns offered by banks and building societies. As of 18 February 2026, Moneyfacts reported the current average rate for an easy access savings account at 2.42%. Any further cuts in the base rate are likely to compress these returns further. This development could disproportionately affect individuals who rely on interest income from their savings, such as retirees or those on fixed incomes, necessitating a careful review of their financial strategies. Banks often adjust savings rates downwards relatively quickly following a base rate cut, aiming to protect their profit margins.

Global Interest Rate Landscape

In recent years, the UK has distinguished itself by maintaining one of the highest interest rates among the G7, a group comprising the world’s seven largest advanced economies. This position reflects the unique challenges the UK has faced in combating persistent inflation and navigating post-Brexit economic adjustments.

Globally, other major central banks have also been grappling with similar inflationary pressures and are now navigating their own easing cycles. In June 2024, the European Central Bank (ECB) initiated its own rate-cutting cycle for the eurozone, reducing its main interest rate from an all-time high of 4%. This move was driven by a combination of falling inflation and concerns about economic slowdown across the Eurozone.

Across the Atlantic, the Federal Reserve in the United States has also been under scrutiny. Former President Trump had repeatedly criticised the Fed for not cutting rates earlier, arguing that higher rates were hindering economic growth. The article notes that President Trump has picked Kevin Warsh to lead the Fed when current chairman Jerome Powell’s four-year term concludes in May 2026. This potential leadership change could signal a shift in the Fed’s future monetary policy approach, potentially aligning with calls for more aggressive rate cuts, depending on the economic data and the new chairman’s philosophy. The broader global trend, therefore, appears to be moving towards monetary easing, though the pace and extent vary significantly based on individual country economic conditions and policy mandates. The UK’s path will continue to be influenced by both domestic factors and these international developments.