This data point critically underscores the inherent fragility of the British economy even before the full geopolitical ramifications of the escalating Middle East conflict began to unfold. The "US-Israeli war with Iran," as described, has rapidly triggered a major energy shock, sending tremors through global markets and threatening a ripple effect that could impact economies worldwide. Such conflicts typically lead to increased oil prices due to supply concerns and heightened geopolitical risk, directly affecting transport costs, manufacturing inputs, and household utility bills. The longer this volatile situation persists, the more profound and likely its adverse effects will be on the UK economy, a warning recently reiterated by Prime Minister Sir Keir Starmer.

While many UK households are shielded from immediate increases in energy prices by Ofgem’s energy price cap, which holds until July, the impact of rising global energy costs is already being keenly felt elsewhere. Fuel costs at the petrol pump have surged, directly impacting commuters and businesses reliant on transport. Similarly, households using heating oil, often in rural areas, have seen their expenses climb sharply. These inflationary pressures pose a significant threat to the Bank of England’s efforts to steer inflation back towards its 2% target, a goal that, prior to the conflict, was largely considered achievable by spring. A sustained period of high energy prices could disrupt supply chains, increase production costs for businesses, and ultimately lead to a broader rise in consumer prices, eroding purchasing power.

If the conflict in the Middle East is prolonged, economists warn that it risks severely dampening household spending, which is a key driver of economic growth. Reduced disposable income due to higher energy and fuel costs, coupled with a potential tightening of credit conditions, could lead consumers to cut back on non-essential expenditures. This scenario directly jeopardises Labour’s stated economic priority to grow the economy, potentially making it harder to fund public services and improve living standards.

Chancellor Rachel Reeves, commenting on the figures, maintained that Labour’s economic plan remains "the right one." She acknowledged the challenges posed by the "uncertain world" but expressed confidence in the government’s strategy. "We are building a stronger and more secure economy by cutting the cost of living, cutting national debt and creating the conditions for growth to make all parts of the country better off," Reeves stated. This plan typically involves targeted fiscal measures, prudent public spending, and initiatives aimed at boosting productivity and investment across various regions. The government’s challenge now is to demonstrate the resilience of this strategy in the face of unforeseen global crises.

Conversely, Shadow Chancellor Sir Mel Stride launched a scathing critique, attributing the UK’s vulnerability to the Iran war’s potential ramifications to Labour’s "economic mismanagement." He argued that the government’s policies had left the nation ill-prepared for such external shocks. Stride called for immediate policy adjustments, urging the government to "axe the fuel tax," which would provide direct relief to motorists and businesses. He also advocated for "backing North Sea oil and gas" to enhance domestic energy security and reduce reliance on volatile international markets. Furthermore, he pressed for a "proper plan to cut the deficit and get the benefits bill down," suggesting a focus on fiscal consolidation and welfare reform as necessary steps to strengthen the UK’s economic foundations. These proposals highlight a clear ideological divide on how best to navigate the current economic turbulence.

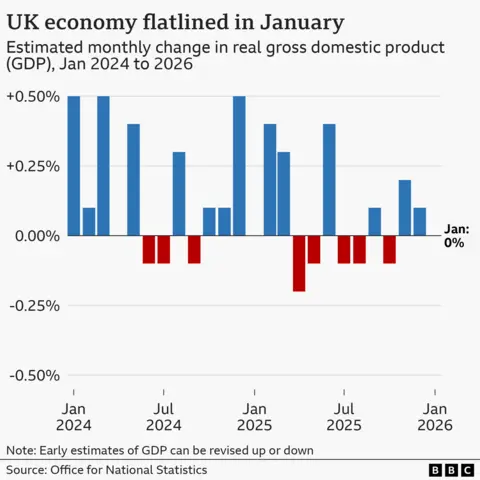

A closer examination of the ONS data reveals the specific sectors contributing to January’s stagnant growth. The services sector, which constitutes the largest part of the UK economy, exhibited no growth at all. This was largely attributed to a decline in consumer-facing services, with "eating out in restaurants" specifically highlighted as a segment that suffered. This suggests a cautious consumer sentiment, possibly influenced by lingering inflationary concerns and the broader economic outlook. Production, encompassing manufacturing, mining, and energy supply, saw a slight contraction of 0.1%, indicating headwinds for industrial output. In contrast, the construction sector proved to be a relative bright spot, growing by 0.2%, potentially driven by ongoing infrastructure projects or a slight rebound in housebuilding activity, though this was insufficient to offset weaknesses elsewhere.

Economic momentum had already begun to wane in the latter half of the previous year. Consumers, grappling with the persistent cost-of-living crisis and anxieties surrounding potential tax increases or job insecurity, demonstrated a tendency to rein in spending. This cautious behaviour had already started to impact overall economic activity. When viewed over a slightly longer period, the three months to January, which offers a less volatile measure compared to monthly figures, saw Gross Domestic Product (GDP) grow by 0.2%. This was a marginal improvement from the 0.1% growth recorded in the three months to December, suggesting a very gradual, almost imperceptible, upward trend before the latest geopolitical events.

In its Spring Statement in March, the Office for Budget Responsibility (OBR), the government’s independent fiscal watchdog, had already revised down its prediction for the UK’s economic growth this year. The forecast was cut from 1.4% to 1.1%, reflecting a more pessimistic outlook even prior to the full impact of the Iran conflict. This downgrade indicated underlying structural challenges and a slower-than-expected recovery path for the UK economy.

Yael Selfin, chief economist at KPMG UK, offered a stark assessment, stating that growth was "likely to remain elusive" for the foreseeable future. She emphasized that the UK economy had commenced the year "on the back foot," and anticipated further weakening of activity, largely due to the "sharply rising energy prices" stemming from the Middle East crisis. Selfin also pointed out that government borrowing costs have climbed in recent weeks, complicating fiscal policy decisions. Before the conflict, financial markets had widely expected the Bank of England to begin cutting interest rates as early as March, providing some relief to borrowers and stimulating investment. However, these expectations have now largely shifted, with analysts widely predicting the Bank will hold interest rates steady at its upcoming meeting next week.

The decision to keep interest rates higher for longer, while potentially necessary to combat inflation, will act as a significant "headwind" for businesses, Selfin added. The dual challenge of weaker growth prospects and escalating operational costs means that firms are increasingly likely to scale back their investment plans. This reduction in investment could stifle innovation, limit job creation, and impede long-term productivity improvements, further entrenching the UK’s economic challenges. The confluence of domestic stagnation and severe external shocks presents a formidable test for policymakers and businesses alike, demanding agile responses to navigate an increasingly uncertain global economic landscape.